DEBT COUNSELLING

What Is Debt Counselling?

Debt Counselling was introduced in South Africa by the National Credit Act in 2007. It was established to help over-indebted consumers develop a repayment plan that is affordable yet also acceptable to all Credit Providers.

The Debt Counselling process is also known as:

Debt Review

Debt Mediation

Debt Relief

Debt Consolidation

What Is The Difference Between Debt Counselling and Debt Review?

No, there is no difference between Debt Review and Debt Counselling. No matter which term you are familiar with, they are the same thing. Within the industry, Debt Review is more commonly used.

What Is A Debt Counsellor?

A Debt Counsellor is a person that speaks to your creditors to negotiate your payment plan and assists you through the entire process from start to finish – including going to court on your behalf when, and if, required.

Debt Counsellors have to be registered with the National Credit Regulator (NCR). To be registered, they have to successfully complete the training course that the NCR runs for Debt Counsellors and meet the competency requirements as set out by the NCR.

At Basson Debt Counsellors (BDC) we pride ourselves on being available to our clients for face-to-face, virtual or telephonic meetings whenever required. Our mission at BDC is to become the best debt review company in South Africa and we can assure you that you are not alone when you go through the Debt Counselling process with us.

What Does A Debt Counsellor Do?

Determining the full extent of the client’s debt

Determining the client’s income

Providing Debt Counselling that:

o Provides an acceptable standard of living for the client, according to affordability, while the client repays their debt

o Restructuring the client’s debt by negotiating with creditors and securing lower interest rates where possible with lower monthly instalments

Providing payment plans that are acceptable to the client’s creditors

Have the payment plan/s confirmed by a Court or the Consumer Tribunal

Distribute the client’s ONE monthly payment to all agreed creditors through an NCR-accredited PDA

Providing the client with a monthly Distribution Statement

Providing the client with a Clearance Certificate once all debt has been settled

Who Is Responsible For Payment Distribution To Your Creditors

According to NCR regulations, Debt Counsellors have to use accredited Payment Distribution Agencies, also known as PDAs, to distribute your payments to the creditors you owe money to.

It is important to remember that Debt Counsellors can NOT, under any circumstances, distribute your funds to your creditors.

What Are The Pros and Cons Of Debt Counselling?

People often find themselves in financial trouble when they borrow more money than they can reasonably afford to pay back. If you find yourself in this situation, Basson Debt Counsellors can help you.

As with most things in life, there are Pros and Cons that you need to consider before taking the first steps toward Financial Freedom.

Pros

Creditors cannot take legal action against you when you are in Debt Counselling

You do NOT have a permanent record of undergoing Debt Counselling

You only make ONE monthly payment

The Debt Counsellor will ensure that your basic needs are met first, before making provision for your debts

You will never be required to pay more than you can afford

The fees are set by law

You will no longer be called by people demanding money from you

Cons

You cannot make more credit while you are under Debt Counselling

There are some costs involved but the fees are set by law

You may take longer to pay off your debt because of lowered monthly payments

Should I Consider Debt Counselling?

Yes, you should consider Debt Counselling if you are over-indebted. The sad reality is that most people do not understand what it means to be OR when they are, over-indebted.

What Is Over-Indebtedness?

If you are unable to pay all your debts on time OR are stressed to the point of losing sleep over your debt, you are over-indebted.

The best advice anyone can ever give you is this – Get help before it is too late! Here is how you know you are over-indebted:

You can NOT pay your debts on time and as agreed with your creditor

You use an overdraft or credit card to pay your debts and buy food and other monthly necessities

You have to borrow money to pay your debt

You do not make all your monthly payments to some of your creditors

You are receiving letters of demand and summonses from creditors and lawyers

You have had judgements granted against you by your creditors

How To Avoid Becoming Over-Indebted

The most important thing to remember is that although we would all like to drive a fancy car and live in a big house, sometimes that is not a possibility. Part of being financially responsible is knowing when you can OR can NOT afford something.

Buying clothing on an account can be a very convenient way of shopping, but only if you know you will be able to pay the account at the end of the month. A lot of stores offer 6-month interest-free payment options. The monthly payment is a bit higher but this is still a much better option than having interest added to an account and taking longer (12 months plus) to pay back your debt and the interest that has been added.

Here are some ways you can avoid becoming over-indebted:

Do a monthly budget and stick to it

Where possible, pay cash for all your purchases

For larger purchases, save money until you can afford to buy it

Live within your means – Be honest when you apply for credit. You will only hurt yourself if you are unable to afford the repayments

Ensure you pay your creditors on time as additional payments could be added due to late and non-payment

Do not be afraid to say NO if you can NOT afford something

Consider how an interest rate hike could affect the cost of your repayment

Do NOT stand as guarantor OR surety for anyone

Do NOT wait till it is too late to contact BDC

Who Can Apply For Debt Counselling?

You can apply for Debt Counselling when:

You are struggling to pay your monthly debt obligations

You have a monthly income that can be distributed to your creditors from one reduced monthly payment

If you are married In Community Of Property you must apply for Debt Counselling together

When your Credit Score has been negatively affected by the amount of debt you have

When Is It Too Late To Apply For Debt Review?

It is unfortunate that a lot of people try to hang on to hope instead of looking for help from a Debt Counsellor. This does not help your situation. In fact, it may be putting you in more financial jeopardy than you realise.

The saddest part of being a Debt Counsellor is when someone desperately needs help with their debt, but there is nothing that can be done for them because they waited too long before looking for help.

Here is a list of the reasons why a Debt Counsellor would NOT be able to help you:

If you do NOT have a fixed income

If your income is too low and a reasonable offer can NOT be made to your creditors

Once legal action has commenced, that/those account/s can NOT be included – judgement, summons etc.

Remember, once you have started the Debt Counselling process, your creditors can NOT issue you with a summons and they must act in good faith and take part in the Debt Counselling process. |

Is There A Limit On The Amount Of Debt I Can Place Under Debt Counselling?

No, there is NO limit to the amount of debt you can place under Debt Counselling in South Africa. However, you have to be able to meet the monthly payment plan that is negotiated with your creditors on your behalf.

What Do I Need To Apply For Debt Counselling?

Email, visit or phone Basson Debt Counsellors OR complete a call-back form

A copy of your salary slip

South African Identity Document – This can only be handed over with the client’s consent

Do I Have To Have A Job To Go Under Debt Counselling?

No, you do not have to be employed to go under Debt Counselling BUT you DO have to have a regular (monthly) income. The income also has to be of a sufficient amount to be able to pay the monthly repayment that the Debt Counsellor has negotiated for you.

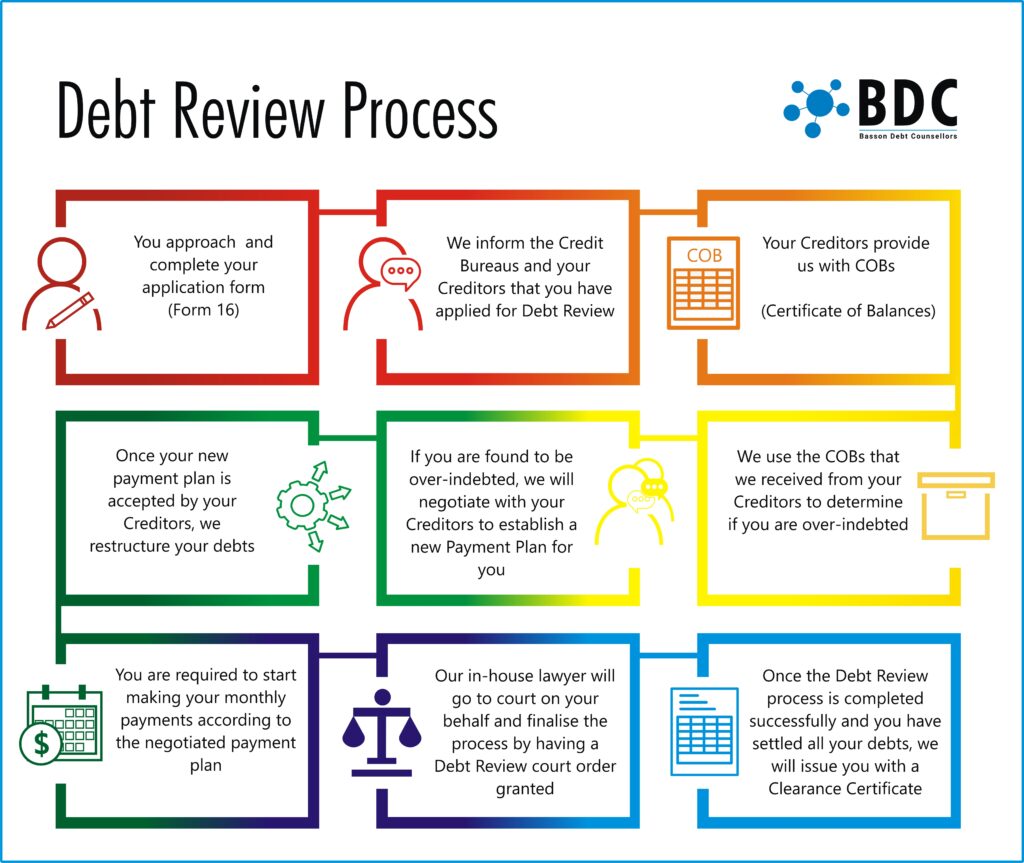

What Is The Process Once I Have Applied For Debt Review?

Here is a step-by-step guide to applying for and going through Debt Review:

Apply in person, by email or by telephone with BDC

We notify your creditors

We inform Credit Bureaus that you are under Debt Counselling to protect you

We negotiate with your creditors

We apply on your behalf for an Order Of Court OR Consumer Tribunal Order

We restructure your debt into ONE Monthly Payment for the duration of your Debt Counselling

We send you a Monthly Distribution Statement

You stay in contact with your Debt Counsellor and ask any questions you may have

BDC supplies you with a Monthly Distribution Statement

We supply you with a Clearance Certificate once your Debt Counselling journey is complete

Do My Creditors Have To Negotiate With My Debt Counsellor?

Yes, if there is a credit agreement in place the creditor has to negotiate with the Debt Counsellor.

If you owe money to the municipality, doctors etc. they may be willing to negotiate with your Debt Counsellor, and often do, but as there is no credit agreement in place, they do not have to.

Can I Apply For Credit While I Am Under Debt Counselling?

No, you can NOT apply for credit when you are under Debt Counselling. The reasons are simple, your Debt Counsellor has restructured your payment plan so as to satisfy your living expenses ensuring that there is no reason for you to have to apply for credit.

Apart from this very obvious reason, you are also prevented BY LAW from obtaining any further credit while under Debt Counselling.

Can I Use My Credit Card While Under Debt Counselling?

No, you can NOT use your credit card while under Debt Counselling. You do not lose your credit card, but you will not be able to access the credit available on it as stated by law. Once you have received your Clearance Certificate you will be allowed to access credit again.

Can I Include My Doctor/School Fees/Cell Phone In My Debt Counselling?

Creditors, such as Doctors, Schools, Electricity Bills, Pharmacy Accounts, Cell Phone Accounts etc. are NOT included in Debt Counselling. This is because there is no credit agreement in place with these accounts. However, it is to their benefit to participate in the process, therefore they usually choose to do so.

Does My Spouse Have To Go Under Debt Review With Me?

Yes, if you are married In Community Of Property, your spouse will have to go under Debt Counselling with you.

When people marry In Community Of Property, they marry each other’s financial status too. This means the good and the bad. Yes, your spouse may be financially stable when you get married but as soon as things go wrong and the debt starts to build, you are married to your spouse’s debts too. You are essentially classified as a single entity according to the law.

If you are Married In Community Of Property, you and your spouse have to sign the Debt Counselling application form OR it will be invalid. Once you have both signed the application form, you and your spouse will remain responsible for the repayment of the debt and will both stay under Debt Counselling until all the debt has been repaid.

It is important to speak to your partner, openly and honestly, about finances before you get married. Getting married Out Of Community Of Property does NOT make you any less married, but it does allow you some form of financial protection.

Will I Be Blacklisted If I Go Under Debt Counselling?

No, you will NOT be Blacklisted if you decide to undergo Debt Counselling. Going under Debt Counselling actually protects you from being Blacklisted as no creditor can serve you with a summons once you start the Debt Counselling process and maintain your monthly payment.

What Does It Mean To Be Blacklisted?

The term Blacklisted is used when describing someone with a negative OR “impaired” credit record. When you do not make your agreed-upon payments to creditors, they notify other creditors to be careful about giving you credit by recording your negative payment history with various credit bureaus.

Will I Be Able To Get Credit Again After I Have Been In Debt Counselling?

Yes, once you have successfully completed the Debt Counselling process you can apply for credit again. Your Debt Counsellor will send a Clearance Certificate to your creditors, the credit bureau and also notify the NCR (National Credit Regulator) and they will remove the ‘Under Debt Review’ flag from your profile. It is for this reason that you will be allowed to apply for credit once again. In other words, you will be able to apply for a bond or car finance with no negative effects from the Debt Counselling process.

It is important to remember that it may take a bit of time to build up your Credit Score again as you would not have had any credit for the duration of your Debt Counselling. This is a small price to pay for the peace of mind that comes with being debt-free.

Will I Be Penalised For Having Been Under Debt Counselling?

No, you will NOT be penalised for having successfully completed the Debt Counselling process. It is important to note that most creditors do not see the Debt Review process as a negative. Instead, they see that the consumer (you) took responsibility for the money owed and successfully settled the outstanding amount/s as agreed with your Debt Counsellor.

How Much Does It Cost To Be Under Debt Review?

A reasonable legal fee goes to the lawyer who drafts the court application and attends the hearing on your behalf. However, this is built into the monthly payments and is NOT a separate fee

Your first monthly payment will go to the Debt Counsellor. This is capped at R8 000 (Can not be more than R8 000). This is to cover all the work that the Debt Counsellor has done to date

5% Of your monthly instalment goes to the Debt Counsellor for after-care. This is capped at R450. This means it can NOT exceed R450 per month

There is a fee for the distribution of funds to your creditors, but this is dependent on the number of accounts being paid from each monthly payment

All these fees are built into your monthly payments and should never be requested or paid separately. All fees are accurate at the time of posting. |

What Are Consumers' Rights And Responsibilities On Debt Counselling?

As with everything in life, you, the consumer, have rights when it comes to applying for Debt Counselling. It is important to remember that with rights come responsibilities too. Here is a list of both your rights and responsibilities with regard to Debt Counselling:

Consumer Rights:

You have the right to apply for Debt Counselling

You have a right to request, and be provided with, reasons if your application is rejected

You have a right to be supplied with a written disclosure of fees before you apply for Debt Counselling

You have a right to full disclosure of the process before you apply

You have a right to receive a distribution statement from your Debt Counsellor

Consumer Responsibilities:

You have the responsibility to make sure that you give full and correct information regarding your finances to your Debt Counsellor

You have the responsibility to pay your monthly repayment as agreed with your creditors and Debt Counsellor

You have the responsibility to follow up on your monthly payments or any questions you may have – Do NOT guess – Always ask

You have the responsibility to make sure that YOU understand the Debt Counselling process, fees and how it impacts your life

Do Debt Counsellors Have To Belong To A Professional Body?

Yes, all Debt Counsellors have to belong to the NCR (National Credit Regulator). There are no exceptions to this. Basson Debt Counsellors (BDC) is registered with the NCR and has been since 2009.

BDC were the first Debt Counsellors to successfully apply for a Debt Counselling Court Order in Cape Town. |

Signing up with BDC for Debt Counselling is THE BEST decision you can make for yourself and your family. Your decision is also backed by the knowledge that you are in the capable hands of experienced and professional Debt Counsellors who want to see YOU succeed.