Contents of the National Credit Act (NCA)

The laws that influence the over-indebted consumer

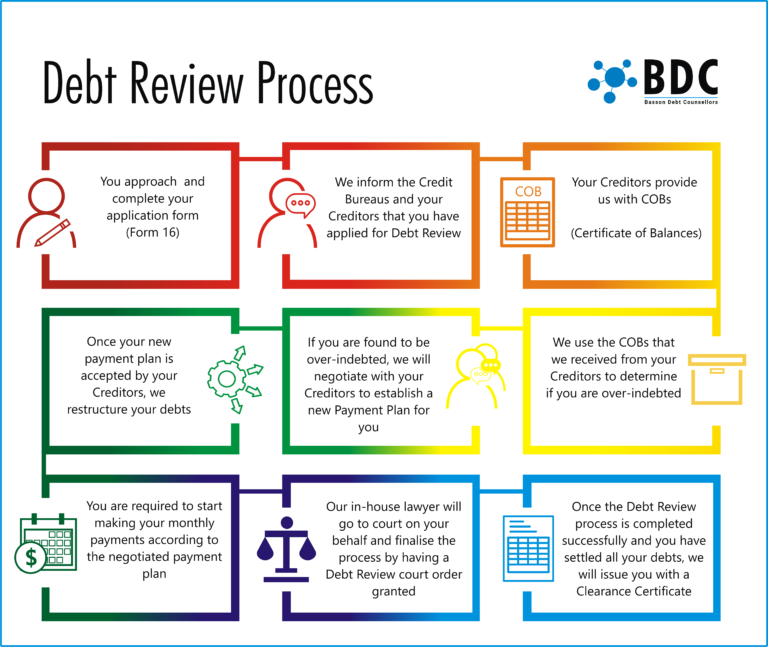

How a consumer can apply for Debt Review

When a consumer can apply for Debt Review

How to read Credit Bureau Reports

How to interpret Credit Bureau Reports

What the term Reckless Lending means

How to draft a Consent Order

How to monitor their clients’ payments

When to issue a Clearance Certificate

How to issue a Clearance Certificate